The Reverse mortgages are like magic keys that help you find hidden wealth plus treasure in your Florida house. It is not about uncovering secret wealth and treasure but it can offer financial stability, allowing you to fully appreciate your elderly years.

Therefore, how does a reverse mortgage work in Florida? Actually it is not that complicated. Designed specifically for homeowners 62 years of age and above this type of loan helps them access the equity hidden away in their houses without having to sell the place they have called home for so long.

Table of Contents

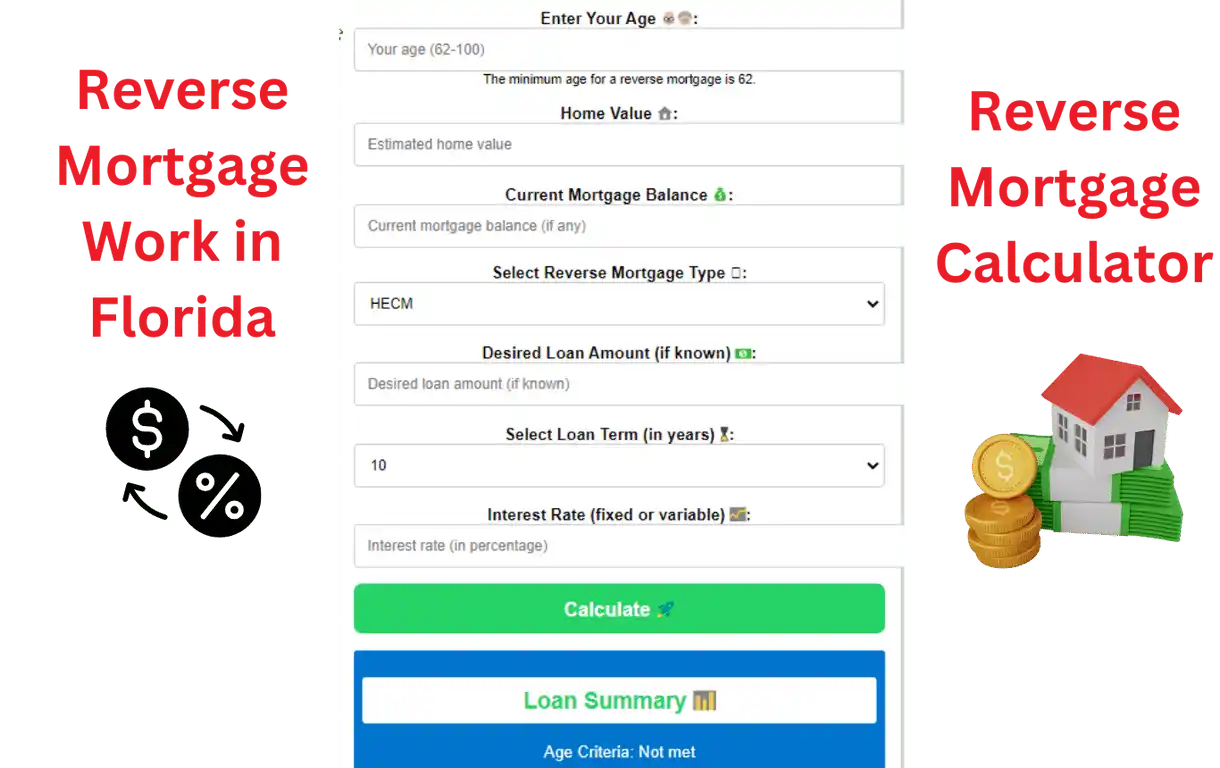

ToggleHow to Use:

- Enter your age.

- Enter the estimated value of your home.

- Enter your current mortgage balance (if any).

- Select the type of reverse mortgage you are interested in.

- Enter your desired loan amount (if known).

- Select the loan term (in years).

- Enter the interest rate (fixed or variable).

- Click the “Calculate” button.

Disclaimer:

This calculator and guide How Does a Reverse Mortgage Work in Florida is for informational purposes only and is not a substitute for professional financial advice. Please consult with a qualified financial advisor to discuss your options and determine the best reverse mortgage solution for you.

Reverse Mortgage Calculator 🇺🇸

Loan Summary 📊

Age Criteria: Not met

Potential Loan Amount: $0.00

Monthly Payments: $0.00

Total Interest Paid: $0.00

Total Repayment Amount: $0.00 The Total Repayment Amount is the sum of the Potential Loan Amount and the Total Interest Paid.

Understanding of Reverse Mortgage

What is Reverse Mortgage:

A reverse mortgage is a specific financial opportunity for home owners primarily those 65 years of age or above. It enables individuals or home owners to make use of the equity in their houses without having to pay a monthly mortgage. It is similar to turning the conventional mortgage concept on its head. Instead of having to pay you receive a payment depending on the value of your house, particularly if you are older62 or older.

Reverse Mortgage works in Florida

How Does a Reverse Mortgage Work in Florida Step by step:

Step 1: Verify Your Eligibility

- You must be 62 years old or older.

- A Florida house must be your principal residence and must be owned by you.

Step 2: Information Gathering

- Gather information about your house, such as its present mortgage status and worth.

Step 3: HUD Counseling

- Contact a HUD-approved counselor in Florida to learn about the reverse mortgage ins and outs. This step ensures you are full or partially aware of all the terms and consequences.

Step 4: Lender Selection

- Find a reputable lender in Florida. It is a important to research different lenders to see who offers the best deal.

Step 5: Application Submission

- Complete the application with your chosen lender. They will guide you through the process including property appraisals and financial assessments.

Step 6: Evaluation and Assessment

- A home valuer determines the worth of your house and to make sure it meets safety regulations and all security rules inspections may be required.

Step 7: Approval and Underwriting

- Lender examines your application and details about the property. They will inform you of the maximum amount or equity you can borrow as soon as you are accepted.

Step 8: Closing the Loan

- You will get your money once you sign the loan agreements. It is available to you as a line of credit a lump sum, monthly smoothly installments and or a combination of these.

Step 9: Financial Responsibilities

- Remember that you are still in charge of keeping up with home maintenance home owner insurance and property taxes.

Types of Reverse Mortgages in Florida

Here are three primary forms of reverse mortgages in Florida:

- Home Equity Conversion Mortgage (HECM): These are the most common and are insured by Federal Housing Administration (FHA). You can pick how you want your money plus wealth.

- Proprietary Reverse Mortgages: A few lenders offer these without FHA insurance. They work well if your home is worth a lot.

- Single-Purpose Reverse Mortgages: Specific groups provide these for specific things like property taxes or fixing your home.

Fees and Expenses of Reverse Mortgages

It is imperative to gain comprehensive insight into the financial intricacies surrounding reverse mortgages. An exploration of the associated charges and outlays is as follows:

- Commencement Fee by Lenders: This singular charge encompasses the preliminary expenses borne by lenders, including the instigation of the process.

- Mortgage Safeguarding Premium: This component serves as a protective layer, shielding both you and the lender. Its significance is notably pronounced in the context of specific reverse mortgage variants.

- Residential Evaluation Expenditure: This is the cost you incur for the enlistment of an adept professional to ascertain the valuation of your domicile.

- Cessation Outlays: Analogous to those affiliated with standard mortgages, these encompass a gamut of charges entailed in the loan’s finalization.

- Loan Administration Levies: Certain financial institutions may subject you to a fee for their services, encompassing the management of your loan and its fiscal administration.

- Accrual of Interest: The sum owed experiences gradual amplification due to the accruement of interest and return on investment.

- Counseling Remuneration: It is indispensable to partake in the counsel of an accomplished advisor during this pivotal stage of the comprehensive process.

Exploring Choices for Settling a Reverse Mortgage

Repaying your reverse mortgage becomes a consideration when your primary residence changes. Here we delve into the various alternatives:

- Transferring Ownership: A prevalent route involves relinquishing your abode. By selling your dwelling, the loan balance is effectively addressed using the sale proceeds. Any remaining equity is then apportioned to either you or your heirs.

- Settling the Loan: An alternative approach is to satisfy the loan balance, allowing you to maintain possession of your home.

- Refinancing: In some instances, an opportunity to refinance your reverse mortgage may present itself.

Strategies for Selecting a Reverse Mortgage Lender

Choosing the right lender assumes paramount importance. Here are key strategies to consider:

- Exhaustive Lender Evaluation: Avoid hastily settling for the first lender that comes your way. Conduct comprehensive research, analyze diverse terms, evaluate rates, and scrutinize fees from multiple lenders to ascertain the most favorable agreement.

- FHA Certification Verification: For those contemplating a Home Equity Conversion Mortgage (HECM), ensure that your chosen lender bears the Federal Housing Administration’s (FHA) endorsement.

- Critical Review of Testimonials: Peruse online critiques and endorsements to assess the lender’s standing and performance.

- Inquire In-depth: Do not hesitate to seek clarifications from the lender regarding any ambiguities or apprehensions. A clear comprehension of all clauses and prerequisites is essential.

- Expert Consultation: Leverage the expertise of financial advisors or specialized counselors in the field of reverse mortgages for personalized recommendations.

The process of designating a reverse mortgage lender is a weighty decision. Dedicate the time needed to make a judicious choice. By adhering to these measures and considering the array of possibilities you can detailed on a secure and congruent reverse mortgage journey in the state of Florida.

Exploring the Realm of Reverse Mortgage Repayment

The obligation of repaying a reverse mortgage materializes when the homeowner relinquishes their primary residence status within the property. The available avenues for repayment encompass the following:

- Selling the Homestead: A prevalent method for settling the reverse mortgage is the sale of the property. The loan balance finds resolution through the proceeds garnered from the sale, with any surplus equity channeling back to the homeowner or their designated heirs.

- Leveraging Personal Finances and Assets: Another avenue entails the utilization of personal financial reserves and assets to satisfy the loan balance, thereby facilitating the retention of the property.

- Exploring Loan Refinancing: A potential alternative is the pursuit of loan refinancing. This route may offer a renewed perspective on the reverse mortgage, delivering flexibility to the homeowner.

Navigating the Labyrinth of Reverse Mortgage Lenders

In the pursuit of a suitable reverse mortgage lender, careful consideration of the following aspects is pivotal:

- Reputation: Opt for a lender adorned with an illustrious reputation, complemented by a profound understanding of the intricate domain of reverse mortgages.

- Examination of Terms and Conditions: The journey toward the ideal lender necessitates an extensive survey of the varied terms and conditions proffered by diverse financial institutions. Selecting the lender whose provisions align most harmoniously with your unique requisites is paramount.

- Scrutinizing the Landscape of Fees and Expenditure: Apprehend the landscape of fees and costs encompassing multiple lenders. A comprehensive appraisal of the financial outlay is conducive to informed decision-making.

People Also Read:

FAQs About Working of Reverse Mortgage

How Do Reverse Mortgages Operate?

An example of a reverse mortgage is when a lender (banks) lends (Means Loans) you money based on the value of your home and your age. Without needing to make regular payments you are still the property owner or home owner. The loan becomes payable when you either pass away or vacate your home permanently.

Who Can Get a Florida Reverse Mortgage?

To meet the eligibility criteria for a Florida reverse mortgage, the following requisites must be satisfied:

- Age: Attainment of the age of 62 or above is mandatory to access the realm of reverse mortgages.

- Property Ownership: Either full ownership of real estate or bearing a nominal mortgage balance is essential.

- Primary Residence Obligation: The property in question must serve as your primary place of abode.

- Financial Competence Showcase: Demonstrating your financial capability to cover maintenance costs, insurance, and property taxes is a prerequisite.

What are the Advantages of a Reverse Mortgage?

- Home Equity Access: Unlock home value without selling or making monthly payments.

- Financial Versatility: Funds for living expenses, mortgages, home improvements, or healthcare.

- Deferred Repayment: Payment only after leaving the home.

- Homeownership Retention: Keep the home as a primary residence.

- Options for Heirs: Choose to repay or sell the property.

What are the Disadvantages of a Reverse Mortgage?

- Accruing Interest: Loan balance grows with accrued interest.

- Initial Costs: Upfront fees and closing expenses.

- Impact on Inheritance: May affect heirs’ inheritance.

- Reduced Home Equity: Diminished home equity as the loan balance grows.

- Complexity: Thorough understanding of terms and implications is essential.

How much money do you get from a reverse mortgage?

The amount you can obtain from a reverse mortgage is influenced by various factors:

Factors influencing reverse mortgage amount:

- Your age

- Property value

- Equity in your home

Borrowing potential increases with:

- Advancing age

- Greater equity

Home valuation’s significant role:

- Typically, 40% to 60% of your home’s appraised value can be accessed.

Consult a professional:

- The best course of action is to speak with an expert reverse mortgage consultant for more in-depth details and customized computations. They can offer you specialized information about your particular financial condition.

Who benefits most from a reverse mortgage?

- Reverse mortgages benefit senior citizens.

- They enable seniors to stay in their homes.

- Seniors can access home equity for retirement income.

- This income can cover expenses like medical bills.

- Eligibility starts at age 62.

- A reverse mortgage provides tax-free income.

- It offers financial flexibility during retirement.

- Seniors can continue residing in their homes.

- Reverse mortgages are a viable retirement finance option.

Can a reverse mortgage be a good thing?

Yes for eligible seniors, a reverse mortgage can offer a myriad of advantages. It is the permits individuals to continue residing in their cherished homes and access their home equity without the worry of making monthly mortgage payments.

A reverse mortgage, acting as a vital income source during retirement can serve as a lifeline for seniors with limited assets. It is the flexibility makes it a valuable tool in addressing unexpected financial needs and medical expenses. However it is the most important to acknowledge that it may come with certain drawbacks. We recommend perusing our list to compare the finest Reverse Mortgage Lenders.

What age can you get a reverse mortgage in Florida?

Residents of Florida who are interested in applying for a reverse mortgage must be at least 62 years old (Age >=62).

Reverse mortgages are actually designed specifically for senior citizens, offering the security of income needed for a happy retirement. Under federal restrictions eligibility is limited to Floridians who are 62 years of age or older (62 Plus age). Seniors in their golden years might live better thanks to this exclusive financial option.

Can you put a 2nd mortgage behind a reverse mortgage?

The answer is no a reverse mortgage cannot be financed by a second mortgage.

Although debtors are not usually prohibited from obtaining additional financing by reverse mortgages, it is not common to find a lender who is ready to secure a loan behind a reverse mortgage. There are, though, some exclusions, particularly with regard to financing for house renovation.

[…] How Does a Reverse Mortgage Work in Florida […]